Today’s post is dedicated to my north star goal of achieving a zero revolving balance on the three credit cards I used to fund my multimedia dreams over the past three-plus years. It won’t be easy, but I’m committed to achieving my mission. My planning is divided into four phases of various difficulty: (1) admitting I have a problem (2) stopping the underlying problematic behavior (3) making a plan and (4) implementing the plan.

(1) Admitting I have a problem:

It took me months and months to admit to myself and others that I had a problem with credit card debt accumulation. After all, without a problem, why endeavor to change a behavior?

(2) Stopping the behavior:

It has taken about a year to get from self-acknowledgment to the point where I was able to “hide the credit cards from myself” to stop problematic multimedia purchases + unnecessary luxury purchasing behavior.

(3) Identifying and customizing a multiple credit card repayment plan that works with my goals and lifestyle:

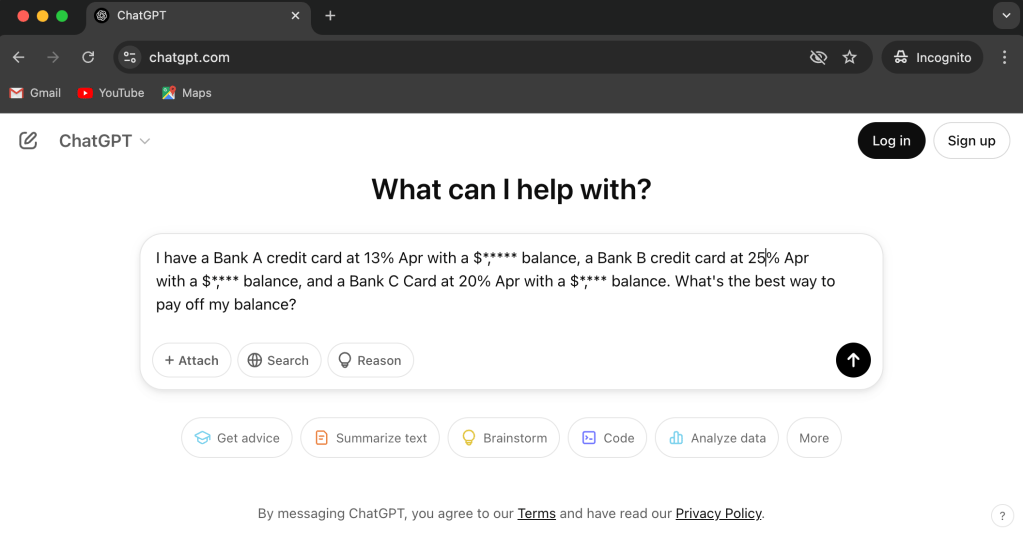

Since this post is being written in 2025, it should come as no surprise that I turned to ChatGPT, from artificial intelligence company OpenAI, to help define the best credit card repayment strategy based on my current principal and interest rates (APR).

The AI identified two options: the “debt avalanche” method, vs. the “snowball” method (hint: I chose “debt avalanche” to start March 2025 strong):

You have a total credit card debt of $***** spread across three cards with different interest rates. The best approach to paying off your debt depends on your financial goals and cash flow. Here are two strategies:

1. Debt Avalanche (Best for Paying Less Interest)

This method prioritizes the highest-interest debt first, minimizing the total interest paid over time.

- Pay the minimum payments on all three credit cards.

- Put all extra payments toward “Highest Interest Rate Card” (25% APR).

- Once “Highest Interest Rate Card” is paid off, focus on the “Second Highest Interest Rate Card” (20% APR).

- Finally, tackle the “Lowest Interest Rate Card” (13% APR).

✅ Pros: You’ll pay less interest over time.

⛔ Cons: It may take longer to see a balance disappear, which can feel discouraging.

2. Debt Snowball (Best for Motivation)

This method prioritizes paying off the smallest balance first, creating psychological momentum.

- Pay minimums on all three cards.

- Put extra payments toward the “Second Highest Interest Rate Card” which has the lowest balance ($*,*** balance).

- Once that card is paid off, roll payments into the “Highest Interest Rate Card” ($*,*** balance).

- Lastly, tackle the “Lowest Interest Rate Card” with the highest balance ($*,*** balance).

✅ Pros: You’ll see faster wins by eliminating cards quickly.

⛔ Cons: You’ll pay more interest in the long run.

Bonus Options to Save Money

- Balance Transfer Card: If you have good credit, transfer high-interest balances to a 0% APR credit card for 12–18 months. This can eliminate interest while you pay off the principal.

- Debt Consolidation Loan: A personal loan with a lower interest rate (e.g., 7-10%) can combine your debts into one payment.

- Negotiate a Lower APR: Call your credit card companies and ask for a lower rate. It doesn’t always work, but even a small reduction can help.

Which Strategy is Best for You?

- If paying the least interest is most important → Debt Avalanche.

- If seeing quick wins keeps you motivated → Debt Snowball.

- If you qualify for a 0% balance transfer or loan → Consider it to save on interest.

For another opinion regarding the Avalanche method vs. the Snowball method, check out a resource provided by Khan Academy’s Personal Finance Course: